What can be predicted with absolute accuracy is that fiat money, fractional-reserve banking, central banks, Keynesian monetary policies, and self-serving politicians will combine to ensure that there will be many more booms and speculative bubbles for future economists and historians to chronicle—Doug French

In this issue

Wilcon Depot’s Dismal 2023 Performance Exposes the Fragile State of the Philippine Consumers and the Real Estate Industry

I. Wilcon’s Sluggish 2023 Performance: A Manifestation of the Real Estate’s Lethargic Conditions

II. Poor Demand from High Vacancy Rates

III. Economic Imbalance: Brisk Inflation of Home Prices Unsupported by Construction Permits

IV. Wilcon’s Stagnant Topline Reflected the Sector’s "Disinflation"

V. Diminishing Returns from Credit-Driven Demand

VI. The Downtrend in Construction and Real Estate GDP

VII. WLCON’s "Build and They Will Come" Strategy

Wilcon Depot’s Dismal 2023 Performance Exposes the Fragile State of the Philippine Consumers and the Real Estate Industry

Wilcon Depot's lethargic 2023 performance manifested the increasing fragility of the Philippines' consumers and the real estate sector.

I. Wilcon’s Sluggish 2023 Performance: A Manifestation of the Real Estate’s Lethargic Conditions

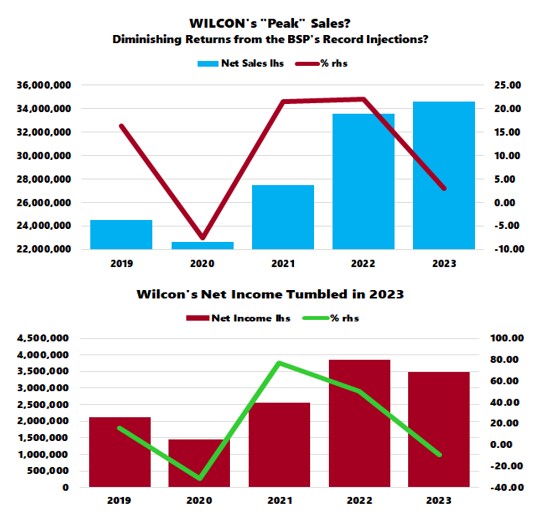

Manila Bulletin, March 22, 2024: Wilcon Depot Inc., the Philippines’ leading home improvement and finishing construction supplies retailer, posted a 9.5 percent drop in net income to P3.48 billion last year as expansion-related expenses resulted in rising operating costs. In a disclosure to the Philippine Stock Exchange (PSE), the firm said net sales improved 3.1 percent to P34.604 billion in 2023 due mainly to the sales generated from the new stores. Gross profit also expanded 4.3 percent to P13.69 billion…“The softness of the market persisted through the fourth quarter, which led to a modest growth in our topline for the year, 100% of which was contributed by the new stores,” said Wilcon Depot President and CEO Lorraine Belo-Cincochan. She noted that “comparable sales dipped by 3.4 percent, impacting directly our net income as operating expenses conversely continued to grow...” “In 2023, on the other hand, there was an apparent slowdown in home improvement spending not only here but globally as well. Despite this slowdown, we continue to pursue our 100-store goal by 2024, a year earlier than initially planned. We believe that we have to be in the best position to serve our market once home improvement spending rekindles,” Belo-Cincochan said. Wilcon opened nine stores in 2023 and ended the year with 90 stores as it also closed one Home Essentials branch and replaced another one with a new depot. (bold mine)

Wilcon Depot [PSE: WLCON], a leading retail chain focusing on home improvement and construction supplies, represents the downstream segment of the real estate industry. Its primary clientele consists of end-users in the industry: individuals, households, commercial enterprises, and public establishments.

Fundamentally, the primary drivers of topline performance are people's time preferences and subjective values, which are expressed through economic and financial conditions. These conditions are influenced by the political climate and are typically measured by occupancy or vacancy rates (aside from affordabiity).

For instance, there should be strong demand for its product line during a productivity-driven boom, characterized by nearly 'full' occupancy rates. However, demand dominated by credit-fueled cycles is fleeting and subject to boom-bust cycles.

Repairing the household/corporate balance sheet is also another example that illustrates the priority of building up savings rather than committing to expenditures—a shift from short-term to long-term preferences.

And the transmission effect, as predicted last July,

…a cutback in new edifices translates to reduced demand for interior furnishing, decorations, and other post-construction activities.

Since the deceleration involved the upstream, the lagged transmission has yet to diffuse into the downstream—WLCON's market. (Prudent Investor, 2023)

Figure 1

The media reported that despite store expansions, WLCON’s sales growth stagnated at +3.1%, while net income declined by 9.5% in 2023.

This slowdown has been admitted by WLCON's CEO:

-The softness of the market persisted through the fourth quarter

-In 2023, on the other hand, there was an apparent slowdown in home improvement spending

There you have it. The soft spot in the real estate sector spilled over to the downstream—Wilcon’s market.

Why so?

II. Poor Demand from High Vacancy Rates

Firstly, real estate vacancy rates remain elevated, spreading from offices to commercial and residential properties.

Although the BSP is aware of this situation, they are left in a quandary:

At present, there seems to be some surprising trends in the residential sector, with prices rising in tandem with vacancies. With the loan portfolio of banks significantly invested in real estate activities, prudence requires a second look. Are housing prices rising because of the rising cost of construction and development? Is this, instead, an indication of generational wealth planning getting ahead of the supply that has been delayed by COVID-19? Or is this a more ominous sign? (BSP-FSCC, 2023) [bold mine]

Figure 2

Nationwide property price growth, based on the BSP's Real Estate Index, nearly halved from 12.9% in Q3 to 6.5% in Q4. (Figure 2, topmost chart) There was little coverage in the media on this.

Paradoxically, this decline in growth emerged amidst robust bank credit expansion to both the supply and demand sides of the sector. (Figure 2, middle window)

III. Economic Imbalance: Brisk Inflation of Home Prices Unsupported by Construction Permits

Secondly, the demand and supply dynamics of the sector appear to diverge.

While property prices surged in early 2023, construction permits have decreased throughout 2023. (Figure 2, lowest image)

Why this critical aberration? Why haven't higher prices prompted substantial participation in a supply buildup to achieve equilibrium?

Could it be that prices were heavily distorted and unsupported by occupancy rates?

IV. Wilcon’s Stagnant Topline Reflected the Sector’s "Disinflation"

Figure 3

Thirdly, as anticipated, the industry and WLCON's demand were reflected in inflation rates. The PSA's Consumer Price Index for furnishing, household equipment, and maintenance resonated with WLCON's sales. (Figure 3, topmost and middle windows)

The takeaway; if price inflation had been instrumental in bolstering WLCON's topline, disinflation, likely through falling use of credit cards, could most upend this dynamic. (Prudent Investor, 2023)

The law of demand went into action: higher prices resulted in lower quantity demanded. Consequently, the industry reduced prices.

This "disinflation" predicament has been shared by WLCON's competitors.

For instance, last March, IKEA Philippines announced up to 50% price discounts on 430 of their most popular products.

V. Diminishing Returns from Credit-Driven Demand

Fourthly, it appears that credit growth, rather than productivity-driven economic conditions, has propelled WLCON's topline.

Diminishing returns from the explosive growth of Universal Commercial Bank credit cards seem to have weighed on WLCON's revenues. Bank credit card growth seems to have plateaued at the 26-30% range. (Figure 3, lowest graph)

The record employment rate last December 2023 hardly helped WLCON’s cause.

Figure 4

Additionally, while bank lending to the construction industry has surged from Q4 2023 to the present, this increase has not yet diffused into the inflation metrics for the construction industry—NCR wholesale (government projects) and retail prices—which have remained depressed. (Figure 4, topmost image)

VI. The Downtrend in Construction and Real Estate GDP

Fifthly, growth in the construction and real estate sectors has been on a downtrend, as evidenced by their respective GDPs. (Figure 4, middle pane)

Similar to the telecom industry, WLCON initially benefited from the shift to work from home and remote work platforms, which significantly increased demand for renovations and home upgrades.

The historic liquidity injections by the BSP also fueled a speculative leverage boom in the real estate industry, which further stimulated spending on household improvements.

The post-lockdown credit-financed "revenge travel" also fueled a spike in demand for the accommodation and food services sector, contributing to its initial growth.

However, beyond competition, the downtrend in the sectoral GDPs could be ominous.

VII. WLCON’s "Build and They Will Come" Strategy

In essence, WLCON's business model appears to be anchored on the popular "build and they will come" strategy—a distortion of Say’s Law.

Besides, with WLCON's slowing net income increasingly dependent on a sustained increase in profit margins, volatile inflation rates, and exchange rates pose increased risks of a profit margin squeeze. (Figure 4, lowest chart)

Yet despite declaring zero debt, the growth of WLCON's lease liabilities (+10.3% Q4) and interest expenses (+11.7 Q4) continues to outpace revenue (-2.11% Q4) and income growth (-14.7% Q4). (Figure 5, topmost and middle visuals)

Interest expenses grew by 17.7% in 2023. (Figure 5, lowest chart)

As noted last July,

The crux, instead of helping boost the bottom line, new stores weighed on WLCON's operations. Additionally, rising interest-bearing lease liabilities continue to gnaw on earnings.

That is to say, slowing financial performance amplifies credit risks—and later, vice versa.

The consensus believes in the eternity of free lunches from the BSP’s easy money regime.

Despite data provided by the government, such as GDP figures, little headway has been made by the consensus in comprehending the adverse impacts of easy money through malinvestments and over-leveraging.

Moreover, everyone seems to think that public spending can only drive consumer growth without considering at whose expense this comes.

Lastly, the consensus has been influenced by the rear-view mirror syndrome or anchoring fallacy—buying into the political flimflam of policy-induced free lunches.

Instead, this cluster of entrepreneurial errant actions from interest rate distortions results in boom-bust cycles. Since actions have consequences, guess what will be the consequence of cumulative errors?

In the end, Wilcon joins the list of consumer companies from different industries, such as Jollibee, Robinsons Retail, and Robinsons Land, reflecting the increasingly fragile state of the Philippine economy.

Based on the April 5th close, Wilcon’s PER was at 18.8—a level that reveals an elevated valuation in the face of a material risk of an income slowdown.

___

References

Douglas French, Early Speculative Bubbles and Increases in the Supply of Money, p.117 August 19,1992 Mises.org

Prudent Investor, Wilcon Depot’s Q2 2023 Sales and Income Growth Slump from Corroding Macroeconomic Forces New Stores, and Disinflation, July 30, 2023

FINANCIAL STABILITY COORDINATION COUNCIL FINANCIAL STABILITY REPORT 2023 Bangko Sentral ng Pilipinas p.38